Insurance Has Its Own Gravity: Policies, Producers, Carriers, and Renewals

If you’re an insurance firm (agency, broker, MGA, carrier distribution team), your world includes:

- Producers and sub-agents.

- Carriers and markets.

- Policies, submissions, quotes, binds, and endorsements.

- Renewals and remarketing.

- Claims and service.

Most insurance shops:

- Have an AMS or policy admin system.

- Use spreadsheets and email as glue around it.

- Struggle to run modern CRM and marketing motions without duplicating data.

HubSpot can be your growth and relationship hub—if it’s placed correctly in your stack.

This article outlines an ideal HubSpot stack for insurance firms:

- What HubSpot should own.

- How it should integrate with your AMS/policy systems.

- Core workflows from lead → quote → policy → renewal.

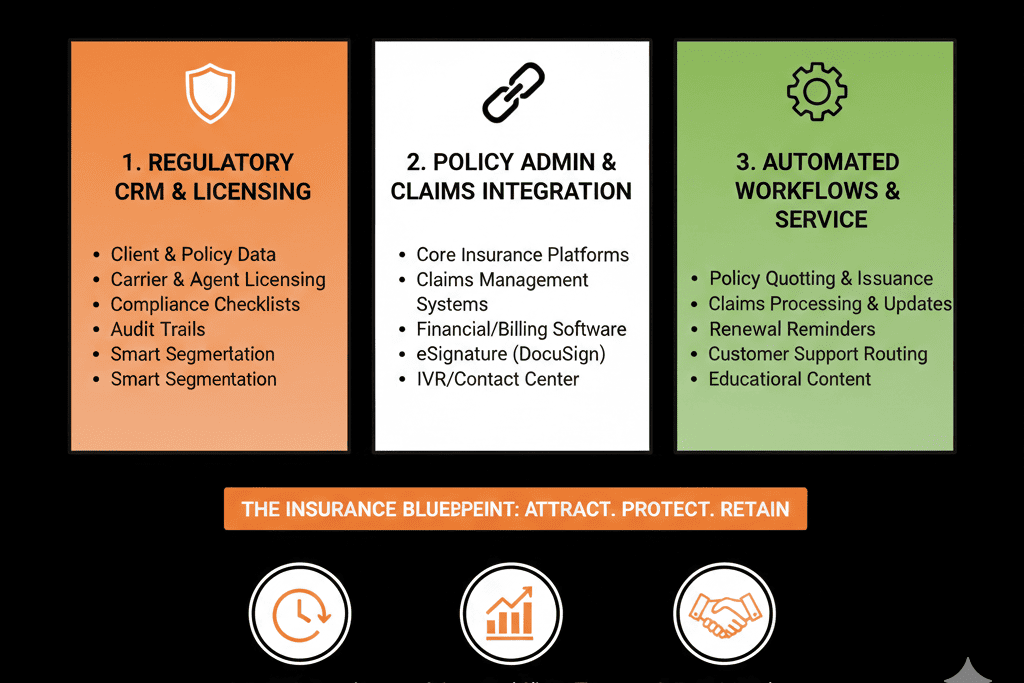

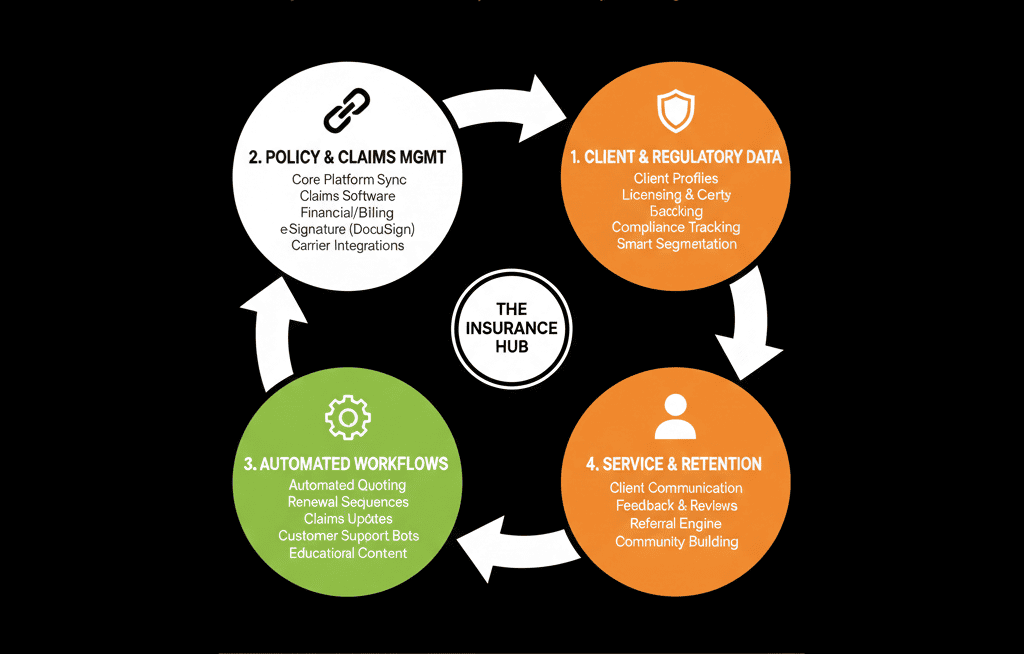

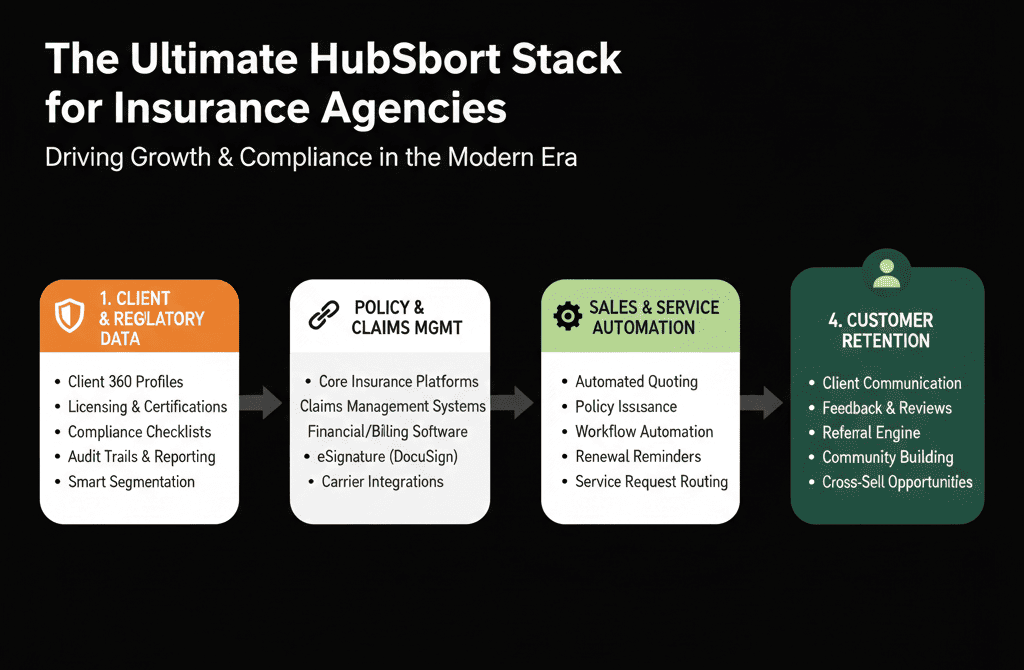

1. HubSpot’s Role in an Insurance Tech Stack

HubSpot should be your system of record for:

- Prospects, clients, producers, and partners (Contacts + Companies).

- Sales and distribution pipeline (submissions, opportunities, quotes in flight).

- Marketing and campaigns (email, events, content).

- Activity history (emails, calls, meetings, tasks).

- High-level premium and commission pipeline and performance reporting.

Your AMS/policy system remains the system of record for:

- Policies, coverages, endorsements, and transactions.

- Policy-level premium, carrier of record, and detailed terms.

- Detailed accounting and reconciliation.

Principle:

HubSpot = sales, distribution, and relationship hub.

AMS/policy = policy and finance system of record.

2. AMS / Policy Admin Integration

Purpose: mirror enough policy information into HubSpot to drive sales and service, without duplicating the AMS.

Typical systems:

- Applied Epic, AMS360, HawkSoft, Vertafore, etc.

- Carrier policy admin systems (for carriers/MGAs).

Integration goals:

Link clients in HubSpot to policies in AMS

Use a unique ID:

- Account/Client ID.

- Policy numbers as needed.

On Companies (and optionally Contacts), store:

- AMS Account ID.

Sync policy summary data

At account level (Company or custom “Policy” object):

- Policy count and types (lines of business in force).

- Total written premium.

- Active vs lapsed policies.

- Renewal dates (earliest/latest).

Optionally, more granular details as required:

- Policy-level premium and line of business.

- Carrier.

Respect data ownership and compliance

- The AMS remains the only place to edit policies.

- HubSpot presents read-only summaries or derived signals for GTM.

Principle:

AMS holds the legal record; HubSpot provides a 360º commercial view for producers, account managers, and leadership.

3. Quoting/Rater Tool Integration

Purpose: connect submissions and quotes to your pipeline view.

Typical tools:

- SEMCI raters, carrier portals, comparative raters, custom quoting tools.

Integration goals:

Track submissions and quotes as deals in HubSpot

Each submission to market:

A Deal representing the opportunity/policy in placement.

Fields on Deals:

- Line of business (Commercial Auto, GL, Property, Life, etc.).

- Submission status (Submitted, Quoted, Declined, Bound).

- Marketed carriers.

- Quoted premium and target premium.

- Producer/CSR/AM.

Mirror rater status into HubSpot

From your rater tool:

- Quoted / Declined / Bound.

- Optionally, carrier quote details summarized.

Drive follow-up and decision workflows

Tasks for:

- Reviewing quotes.

- Presenting options to clients/producers.

- Following up on undecided quotes.

Outcome:

A single picture of submissions and quotes in flight.

Better forecasting and win rate analysis by line, carrier, and producer.

4. Billing and Accounting Integration

Purpose: connect premium and commission numbers into HubSpot.

Typical systems:

- The AMS itself (for agency) or carrier billing systems.

- General ledger: QuickBooks/Xero/Sage/NetSuite, etc.

Integration goals:

Bring high-level financials into HubSpot

On Companies/Deals:

- Written premium.

- Commission (actual or estimated).

- Payment status (optional, summarized).

Use billing data in GTM

Identify:

- Key accounts by premium and profitability.

- Producers contributing the most commission.

- Clients whose premium mix indicates cross-sell opportunities.

Principle:

Detailed accounting remains with AMS/finance; HubSpot sees just enough to drive growth, cross-sell, and account strategy.

5. Claims and Service Touchpoints

Purpose: provide account managers and producers with visibility into client issues and risk.

Typical systems:

- Claim admin platforms or modules within AMS.

- Email/manual logging for smaller organizations.

Integration goals:

Claims summary in HubSpot

On Companies/Accounts:

- Claim count (open & closed).

- Claim severity indicators.

- Recent claim dates.

Use claims data to inform GTM

Renewal planning:

- At-risk accounts flagged early.

Cross-sell/services:

- Risk management services for clients with frequent claims.

- Loss control follow-ups.

Principle:

Claims systems handle adjuster work; HubSpot flags where claims history affects retention, pricing, and cross-sell.

6. Marketing and Producer Communications

Purpose: modernize outreach while honoring compliance and channel structure.

Typical tools:

- HubSpot Marketing Hub.

- Email archiving/compliance systems.

- Websites, landing pages, portals.

Integration/configuration goals:

Segment and target appropriately

Segments by:

- Line of business.

- Role (end client vs producer vs wholesaler vs COI).

- Industry and size.

- Renewal dates.

Campaigns for

- New product launches and carrier appetites.

- Risk management content for specific industries.

- Producer education and updates.

- Cross-sell campaigns (e.g., clients with GL but no Property).

Measure marketing → pipeline impact

Use HubSpot Campaigns to:

Track campaign influence on submissions and bound premium.

Principle:

HubSpot enables targeted, trackable communication to clients, producers, and partners—aligned to actual pipeline and policies.

7. Core HubSpot Workflows for Insurance Firms

To make this stack work, build core workflows inside HubSpot:

Lead & referral intake

Normalize:

- Source (Web, Referral – Client, Referral – Producer, Event, etc.).

- Lifecycle (Lead, Prospect).

- Owner (Producer/CSR).

Submission and quote process

When a new submission comes in:

- Create/Update Deal.

- Set submission status.

- Assign to producer/CSR.

- Trigger rater or market selection steps in external tools.

Policy bound & AMS sync

On “Bound” or “Policy Issued”:

- Sync or create policy in AMS (if not already created).

- Update Deal to Closed Won.

- Attach relevant policy info in HubSpot.

Renewal & remarketing workflows

From AMS → HubSpot:

- Pull renewal dates.

In HubSpot:

- Create Renewal deals X days in advance by line/segment.

- Task producers/AMs for: Account review; remarketing where needed.

Cross-sell and up-sell

From policy summary:

Identify accounts with gaps (e.g., GL but no Property).

Use workflows to:

- Create tasks/opportunities.

- Enroll segments in cross-sell campaigns.

8. Example Ideal Stack Around HubSpot for an Insurance Firm

A solid, practical setup might be:

- HubSpot – CRM, marketing, sales, producer/AM GTM hub.

- AMS/Policy system – Epic, AMS360, HawkSoft, etc., as policy & finance SOR.

- Comparative Rater/Quoting – integrated to sync submission/quote status.

- Accounting – linked to AMS; high-level numbers mirrored in HubSpot.

- Claims system – integrated in summary.

- E-sign – DocuSign/HelloSign for apps, policies, and endorsements.

- Compliance/Archiving – email and data archiving integrated to meet regulatory requirements.

- BI/Data Warehouse – for deeper analytics across AMS + HubSpot.

With:

- HubSpot in the center for: Lead, client, producer, and partner management.

- Pipeline and revenue views.

- Marketing and communication.

- Renewal/cross-sell orchestration.

What You Can Do in the Next 60 Days

If you’re an insurance firm using or considering HubSpot:

Clarify HubSpot’s intended role:

- Producer/agency CRM and GTM engine, not a policy system.

Map your current stack:

- AMS/policy admin.

- Raters/quoting tools.

- Billing/accounting.

- Claims.

- Marketing/email tools.

Prioritize two integration points:

- AMS → HubSpot (policy summary & renewals).

- Rater/quoting → HubSpot (submission/quote status).

Implement/refine these core workflows:

- Lead/referral intake.

- Submission → quote → bound pipeline.

- Renewal & remarketing triggers.

Build 1–2 dashboards:

- New business pipeline by line and producer.

- Renewal pipeline and retention metrics.

Want an Insurance-Specific HubSpot Stack Blueprint?

Insurance is not like SaaS or generic B2B:

- Policies, renewals, carriers, and producer networks change the game.

- AMS systems and regulatory needs make architecture more complex.

Our HubSpot Portal Health Check / HubSpot Audit can:

- Map how your GTM and policy processes run today.

- Propose a realistic, phased HubSpot-centered stack around your AMS and quoting tools.

- Provide a 60–90 day roadmap for integration and workflow improvements.